Medicinal and Toilet Preparations Act, 1955 and Rules

Intended Learning Outcomes

• At the end of this lecture, student will be able to

– Write the introduction and reasons for implementation of the Medicinal and Toilet Preparation Act, 1955

– Describe the objective of Excise Duties Act, 1955

– Define the related terms included in the Excise Duties Act, 1955

Medicinal and Toilet preparations (Excise duties) act, 1955 and Rules

Objectives of Medicinal and Toilet preparations act

• To provide for the collection of levy and duties of excise on medicinal and toilet preparations containing alcohol, narcotic drugs or narcotics

• To provide for uniformity in the rules and rates of Excise duties leviable on such preparations throughout the country

Definitions

• Alcohol means ethyl alcohol of any strength and purity having the chemical composition C2 H5 OH

• Absolute alcohol means ethyl alcohol containing less than 1% by weight of water

• Dutiable Goods means the medicinal and toilet preparations specified in the Schedule as being subject to the duties of excise levied under the Act

• Medicinal Preparation includes all drugs which are a remedy or prescription prepared for internal or external use of human being or animals and all substances intended to be used for or in the treatment, mitigation or prevention of disease in human beings or animals

• Toilet Preparation means any preparation which is intended to cleanse, improve or alter the complexion, hair, skin, or teeth, and includes deodorants and perfumes

• Bonded Manufactory means the premises approved and licensed for the manufacture and storage of medicinal and toilet preparations containing alcohol, opium, Indian hemp or any other narcotic drug or narcotics on which duty has not been paid

• Non-bonded Manufactory means the premises approved and licensed for the manufacture and storage of medicinal and toilet preparations containing alcohol, opium, Indian hemp or any other narcotic drug or narcotics on which duty has been paid

• Denatured Alcohol or denatured spirit means alcohol of any strength which has been rendered unfit for human consumption by the addition of substances approved by the Central Government or by the State Government with approval of the Central Government

• Rectified Spirit means plain denatured alcohol of a strength not less than 50.00 over proof and includes absolute alcohol. It is highly concentrated ethanol which has been purified by means of repeated distillation, a process that is called rectification.

• Restricted Preparation means every medicinal and toilet preparation specified in the Schedule and includes every preparation declared by the Central Government as restricted preparation

• Unrestricted Preparation means any medicinal or toilet preparation containing alcohol but other than restricted preparation or a spurious preparation

What is an Excise?

• Is an inland tax on the sale, or production for sale, of specific goods or a tax on a good produced for sale, or sold, within a country or licenses for specific activities?

• It is different from Customs duties ( border taxes)

• An excise tax is distinguished from a sales tax or VAT in three ways:

• (i) an excise typically applies to a narrower range of products;

• (ii) an excise is typically heavier, accounting for a higher fraction of the retail price of the targeted products; and

• (iii) an excise is typically a per unit tax, costing a specific amount for a volume or unit of the item purchased, whereas a sales tax or VAT is proportional to the price of the good

• An excise is considered an indirect tax, meaning that the producer or seller who pays the tax to the government is expected to try to recover or shift the tax by raising the price paid by the buyer

Central Board of Excise and Customs

• Central Board of Excise and Customs (CBEC) is a part of the Department of Revenue under the Ministry of Finance, Government of India

• It deals with the tasks of formulation of policy concerning levy and collection of Customs & Central Excise duties and Service Tax, prevention of smuggling and administration of matters relating to Customs, Central Excise, Service Tax and Narcotics to the extent under CBEC’s purview

• The Board is the administrative authority for its subordinate organizations, including Custom Houses, Central Excise and Service Tax Commissionerates and the Central Revenues Control Laboratory.

Licensing

• Manufacturing of alcoholic and narcotic preparations can only be undertaken under the authority of a licence granted for this purpose

• A license will be granted only if the applicant holds the requisite license for the manufacture of drugs under the Drugs and Cosmetics act.

• The act also specifies procedures to be followed for the manufacture of Homeopathic and Ayurvedic preparations, removal of goods from bonded labs, interstate movement of preparations etc.

• Application for the licence or for its renewal is to be made to Licensing authority who is the EXCISE COMMISSIONER

• A separate application is to be made if more than one kind of licence is desired

• The application for the licence should be submitted in the prescribed form accompanied with the prescribed fee

• The particulars required to fill in the application for obtaining the licence are:

– Name and address of the applicant and place and site on which the manufacturing unit is situated

– The amount of the capital proposed to be invested in the venture

– Approximate date from which the applicant desires to commence the manufactory

– The number and full description of vats, still and other permanent apparatus and the machinery which the applicant wishes to get together with the maximum quantity of alcohol

– The site and the elevation plans of the manufactory/building and also similar plans for the quarters of the Excise Officer together with relevant records

– The amount on cash or Government Promissory Notes which the applicant is prepared to furnish for the due performance of the conditions on which the licence may be granted

– The kind and number of each licence under the Drugs and Cosmetics Act held by the applicant

– A list of all preparations which the applicant proposes to manufacture and /or those manufactured during the preceding year showing the percentage or proportion of alcohol in preparations or opium, indian hemp or other narcotic drug

Manufacture outside Bond

• Preparations are deemed to be manufactured in bond when they are manufactured in a premise, licensed or approved for this purpose and on which the excise duty has been paid at the time of spirit purchase

• A license is required for undertaking the manufacture of medicinal and toilet preparations without a bond

• The application for the licence should be submitted in the prescribed form accompanied with the prescribed fee at least 2 months before the date of commencement of the manufacture

• The conditions are similar to that of manufacture in bond

Conditions of License

– The form of application and other conditions for license is the same as that of manufacture in bond

– Non- bonded laboratory should be separate from the rest of the business premises and should be used exclusively for the manufacture of spirituous medicinal and toilet preparations

Design and construction of a non-bonded laboratory

A non- bonded lab should consist of the compartments as per the following diagram

- A Spirit Store

- A room for the manufacture of medicinal preparations

- One or more rooms for the storage of finished medicinal preparations

– The manufacture and sale in a non- bonded lab should be conducted between sunrise and sunset only and on days as fixed by the excise commissioner for the purpose.

– There should be only one entrance to the lab and only one door for each of its compartments

– Every window in the bonded premises should be provided with maleable iron rods, not less than 1.9 cm in thickness and set not more than 10 cm apart

– The rods should be embodied in brick work to a depth of atleast 5 cm and covered on the inside with strong netting or expanded metal of a mesh not more than 2.5 cm in diameter in length

– Each room in the lab should bear a board indicating its serial number and purpose

– The pipes from sinks inside the laboratory should be connected to the general drainage of the premises

– The gas and electric connections in the lab should be arranged in such a way that their supply can be cut off at the end of a day’s work

– Permanent vessels should be provided for the storage of alcohol and other narcotic substances received under bond

– All vessels should bear a distinctive serial number and a statement of their full capacity

Manufacture in a non-bonded laboratory

– The essential steps are :

- Obtaining raw spirit from distillery after duty payment

- Manufacture

- Storage of finished preparations

- Returns

1. Obtaining raw spirit from distillery

– Raw spirit is obtained from a distillery approved by the Excise commissioner

– An indent is sent in the prescribed form, countersigned by the officer in charge of the lab ( in Duplicate)

– One copy to the distiller or warehouse keeper and the other to the excise officer in charge of the distillery or warehouse

– Before sending a copy to the officer in charge of the distillery, the manufacturer should pay the excise duty on the alcohol to be purchased

– The treasury challan of the payment should be enclosed with the indent

– The treasury officer shall also send an advice to the Excise officer in charge of the distillery

– After verification of the payment details, the excise officer shall issue the spirit along with a permit covering the issue

– The spirit will then be transferred to the spirit store and entered in the register

2. Manufacture of alcoholic preparations

– The manufacture of preparations from duty paid spirit should be carried out only at the licensed premises

– Each preparation, soon after its manufacture, should be registered and given a distinctive batch number

3. Storage of finished preparations

– All finished preparations should be transferred from the lab to the finished goods store and so arranged that they can be easily checked from the stock register

– Preparations stored in bulk should be measured in the storage vessel nearest to 28.350 ml

– The quantities taken out from time to time should be entered in the stock maintained for the purpose

4. Sampling

– The excise officer of the concerned jurisdiction, without any previous notice to the manufacturer, shall take samples of not less than 10% and more than 15% of the total batches manufactured during the month

– All such samples should be taken personally by the officer in the presence of the manufacturer

– Every sample shall be taken in duplicate and the labels of the bottles should be signed by the officer taking the samples

– The cork of every bottle should be fixed with the seal of the officer

– The manufacturer can also add his seal to the sample bottles

– If the alcoholic content differs by more than 30 proof on either side from the strength declared by the manufacturer, he shall pay a penalty at the rate of 10 times the duty payable

5. Returns

– The manufacturer should maintain up to date and proper accounts of all transactions and deliver them to the concerned officers on the 5th of each month

– Any change in staff should be intimated to the excise commissioner

6. Inspection

– The non-bonded lab shall be open to inspection by officers of the excise department

– It shall be inspected at least once every month

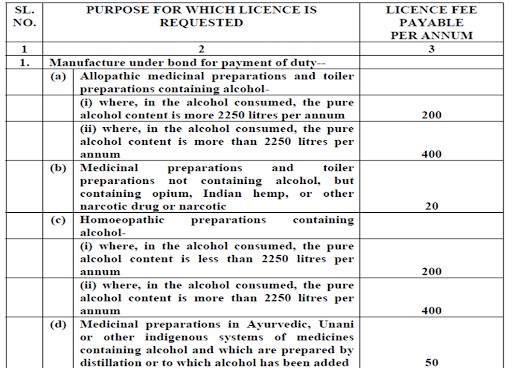

Fees

• The fees to be paid for obtaining a license are:

Offences and Penalties

| OFFENCES | PENALTIES |

|

I. BY LICENSEES |

|

| a) Failure to follow licence conditions/pay duty | Imprisonment up to 6 months or fine up to Rs. 2000 |

| b) Disorderly keeping of stocks or accounts | Fine up to Rs. 2000 |

| c) Illegal sale of dutiable goods | Fine up to Rs. 1000 |

| d) Failure to furnish export proof | Fine up to Rs. 2000 |

| e) Obstruction to officers/ false information | Fine up to Rs. 5000 |

| f) Failure to provide/ maintain weighing or measuring devices | Fine up to Rs. 1000 |

| g) Failure to provide / maintain facilities for locking |

Fine up to Rs. 200 |

|

II. BY EXCISE OFFICERS |

|

| a) Failure to do duty | Imprisonment up to 3 months or fine or both |

| b) Vexatious searches / seizures | Fine up to Rs. 2000 |

| c) Disclosure of information | Fine up to Rs. 1000 |

|

III. BY PUBLIC |

|

| a) Malicious information | Imprisonment up to 2 years or fine upto Rs. 2000or both |

| b) Connivance of owners/ occupiers of land | Imprisonment up to 6 months or fine upto Rs. 500 or both |

Latest amendments

• Amendment of Article 268 (1) (Duties levied by the union but collected by the States): –

– Article 268 (1) provides the provision of levy of stamp duty and excise duty on medicinal and toilet preparation by union government and collection by state (In case of State) or by union (In case of union territory).

– Now, the duties of excise on medicinal and toilet preparation has been omitted and same is been amalgamated in GST.

Manufacture in Bond

• Preparations are deemed to be manufactured in bond when they are manufactured in a premise, licensed or approved for this purpose and on which the duty has not been paid until the finished products are removed from the licensed premises

• Every person interested in manufacturing preparations containing alcohol or other narcotic substances should obtain a license for the Excise Commissioner of the concerned state

• The application for the license should be submitted in the prescribed form accompanied with the prescribed fee at least 2 months before the date of commencement of the manufacture

Licensing

• The particulars required to fill in the application for obtaining the licence are:

– Name and address of the applicant and place and site on which the bonded lab is proposed to be situated

– The amount of the capital proposed to be invested in the venture

– Approximate date from which the applicant desires to commence the manufacture, stating the % of alcohol in each

– The number and full description of vats, still and other permanent apparatus and the machinery which the applicant wishes to get together with the maximum quantity of alcohol to be used

– The site and the elevation plans of the manufactory/building, showing the different rooms, doors and windows, along with similar plans for the quarters of the Excise Officer together with relevant records

– The kind and number of each licence under the Drugs and Cosmetics Act held by the applicant

– In case of a firm, copy of the partnership deed and in the case of companies, the list of directors and managers.

– A list of all preparations which the applicant proposes to manufacture and /or those manufactured during the preceding year showing the percentage or proportion of alcohol in preparations or opium, indian hemp or other narcotic drug

Processing of application

– On receipt of application, the licensing authority will enquire into the

1) The qualifications and experience of the technical personnel involved in the manufacture

2) The equipment of the bonded laboratory

3) Suitability of the proposed building for the establishment of bonded laboratory

4) Applicants financial position

Conditions of License

– If the Excise commissioner is satisfied with the enquiries made, he may issue directions for license to be issued and approve the plans of the building and equipments

– On completion of the construction, the licensing authority will ascertain whether the construction has been done in accordance with the approved plan

– Separate licenses should be obtained for separate premises of business

– If the licensee desires to transfer his business to another person, the transferee should obtain a fresh license which shall be granted free of fee for the residue of the period covered by the original license

– Any transfer in premises should be notified to the licensing authority 10 days in advance and obtain an amended license

– The license is valid for a period of 1 year and should be renewed thereafter

– The application for renewal should be submitted one month before the due date

– The license should be displayed in a prominent place within the premises

– The licensee should allow his premises and goods to be inspected by the licensing authority

– A visit book should be maintained to enter the remarks of the visiting officers

– All invoices and documents related to the business should be maintained

Design and construction of a bonded laboratory

A bonded lab should consist of the compartments as per the following diagram

- A Spirit Store

- A room for the manufacture of medicinal preparations

- One or more rooms for the storage of finished medicinal preparations

- If the manufacture of toilet preparations is also carried on, a separate manufacturing room for these together with a separate room for the storage of finished toilet goods

- Accommodation, with necessary furniture for the excise officer in charge of the bonded lab, near its entrance

– There should be only one entrance to the lab and only one door for each of its compartments

– The lab can be opened only in the presence of the excise officer and during his absence, all the doors should be secured with excise ticket locks

– Every window in the bonded premises should be provided with maleable iron rods, not less than 1.9 cm in thickness and set not more than 10 cm apart

– The rods should be embodied in brick work to a depth of at least 5 cm and covered on the inside with strong netting or expanded metal of a mesh not more than 2.5 cm in diameter in length

– Each room in the lab should bear a board indicating its serial number and purpose

– The pipes from sinks inside the laboratory should be connected to the general drainage of the premises

– The gas and electric connections in the lab should be arranged in such a way that their supply can be cut off at the end of a day’s work

– Permanent vessels should be provided for the storage of alcohol and other narcotic substances received under bond

– All vessels should bear a distinctive serial number and a statement of their full capacity

– All vessels, containing preparations on which duty has not been paid should be secured with excise ticket locks.

Manufacture of preparations in bonded laboratory

– The essential steps are :

- Obtaining raw spirit from a distillery without duty

- Verification of raw spirit by excise officer

- Storage of raw spirit in the raw spirit store

- Manufacture

- Storage of finished preparations

- Issue of preparations from bonded lab

1. Obtaining raw spirit from distillery

– Raw spirit is obtained from a distillery approved by the Excise commissioner

– An indent is sent in the prescribed form, countersigned by the officer in charge of the lab ( in Duplicate)

– The distiller will receive the duplicate copy of the indent and issue the spirit in duly sealed containers along with the advice of consignment to the excise officer in charge of the bonded lab

– There should be no wastage of spirit during transportation from the distillery to the lab

– In case there is a loss of contents due to negligence by the manufacturer, the manufacturer will be asked to pay duty on the total loss in the amount of spirit

– However if the Excise commissioner is satisfied that the loss has occurred despite all care taken by the manufacturer, he may waive off the duty on the lost spirit

2. Verification and storage of raw spirit

– The consignment of the spirit has to be verified in volume and strength by the Excise officer on its arrival in the bonded lab and the amount entered in the register maintained for the purpose

– The spirit will then be stored in the spirit store

3. Manufacture of alcoholic preparations

– Whenever the manufacturer wants to manufacture any preparation, he must calculate the requirements of the spirit and hand it over to the officer in charge

– The officer will then issue the spirit

– Before requesting for the spirit, all the other ingredients of the preparation should be kept ready

– The spirit is then mixed with the ingredients in the presence of the officer in charge

– The finished product is then moved to the finished goods store, measured and stored in the vessels provided for the purpose

– It should also be entered in a register and given a batch number

– The officer in charge may permit the manufacturer to take a sample upto a max of 250 ml from each batch of the finished preparation, free of duty for determination of its alcoholic strength

– A separate account should be entered for samples used for analysis and any amount left over after analysis should be mixed with the main batch

4. Storage of finished preparations

– All finished preparations should be stored in bulk in jars and bottles, each containing not less than 2.25 litres of the preparation

– Every container should be labeled with the name of the preparation, batch number, strength, date of storage and actual content

– Preparations may be issued in containers not less than 50 ml capacity

– The stored preparations should be entered in a stock ledger which should be updated with manufacture of each batch

5. Issue of finished preparations

– Whenever the manufacture wishes to take out any preparation from the bonded lab, he must present an application to the excise officer and pay duty for it

– The officer will check the entries, realize the duty and allow the preparations to be removed from the bonded lab

– Before issue of preparations, an issue pass has to be written out by the Excise officer

Summary

• Use of alcohol for preparation of medicines is necessity.

• Alcohol used either for drinking or manufacture of perfumes is subjected to higher duties than that of used in medicine preparation.

• The Excise Duties Act came in force in 1955.

• For excise duty to be an effective alcohol control measure, duty increases need to increase annually in relation to inflation and income.

• An excise or excise tax is an inland tax

• The objective of the Act is to provide for the collection of levy and duties of excise on medicinal and toilet preparations containing alcohol, narcotic drugs or narcotics

• Alcohol means ethyl alcohol of any strength and purity having the chemical composition C2H5OH

• Medicinal Preparation includes all drugs which are a remedy or prescription prepared for internal or external use of human being or animals and all substances intended to be used for or in the treatment, mitigation or prevention of disease in human beings or animals

For PDF Notes Click on Download Button